Introduction

This article discusses whether the UK should embrace a hydrogen economy or one based on electrification. It draws together evidence from three previous articles on: (i) heavy goods vehicles; (ii) heating buildings; (iii) electricity storage. These are the three applications that are most frequently cited as attractive for future use of hydrogen.

Although the article focusses on the UK, the arguments should apply reasonably well to most other mid-sized developed countries.

Key Take-Aways (TLDR)

- The proposed Green Hydrogen economy is unlikely to be realisable in the UK. An ‘Electron economy’ has a higher likelihood of success.

- For heavy goods vehicles, direct electrification via batteries and electric roads are options with higher Technology Readiness Level (TRL), lower energy consumption, lower carbon emissions and lower costs than hydrogen-powered fuel cell vehicles.

- Heat pumps are a better option for heating buildings than hydrogen boilers. Heat pumps are readily available now. They have lower energy consumption, lower carbon emissions and have much lower fuel costs than hydrogen boilers.

- For electricity storage, Green Hydrogen is unlikely to be able to compete with more efficient alternatives such as cryogenic (liquid air) storage and compressed air storage, which offer almost equivalent energy storage capabilities at lower cost and higher TRL.

- Shifting the energy for lorries and heating to Blue Hydrogen would result in the UK importing and burning an additional 260 TWh of natural gas per year. This would increase natural gas imports by 50% and increase overall consumption by nearly 30%. It would be detrimental to the country’s balance of trade and energy security.

- The push for Hydrogen is likely to delay the international decarbonisation project and undermine efforts to keep the global average temperature less than 1.5 ºC above pre-industrial levels.

The main technical arguments presented in this article are based on three more detailed articles that are available elsewhere on this website:

- [Article 1]: Hydrogen vs electricity for long-haul road freight

- [Article 2]: Hydrogen vs electricity for heating

- [Article 3]: Use of hydrogen for electricity storage

Background

How Urgent is Decarbonisation?

Rapid decarbonisation of all human activities is now imperative. Figure 1, from [1], shows CO2 mitigation paths needed to maintain global temperatures less than 1.5 ºC above pre-industrial levels (as agreed in the Paris agreement in 2015). It shows that Carbon emissions must be reduced steadily to near zero between 2020 and 2040 if the 1.5 ºC target is to be met. If urgent action isn’t taken, just eight more years of emissions at 2020 levels will use-up the remaining Carbon budget. After that, the only possible way to stay under the 1.5 ºC temperature rise will be to extract CO2 from the atmosphere. This is currently completely uncharted territory, with no known way to capture CO2 from air at sufficient scale.

‘Shovel Ready’

On December 4, 2020, Prime Minister Boris Johnson announced plans to reduce UK Carbon emissions by 68% (relative to 1990 levels) by 2030. This target is an admirable milestone on the road to the government’s ‘net zero’ Carbon emissions commitment by 2050. However, the 2030 target brings into sharp focus the need to implement major decarbonisation projects quickly.

Many aspects of decarbonisation of UK systems require large-scale infrastructure construction projects which often take 5-10 years, or more, from conception to commissioning. Consequently, where such large-scale infrastructure is needed for decarbonising the UK’s energy systems – for power generation, fuel manufacture and distribution, vehicle production or grid-scale energy storage systems – construction projects must begin in the next few years. Otherwise there will not be sufficient time to approve, design, procure, build and commission the infrastructure before 2030. This means there is little or no time left for new technologies to be developed… Solutions that can’t be implemented quickly at a large scale must be ruled-out. We must ‘use the tools that are already in the toolbox’.

Conclusion: ‘Shovel ready’ solutions, with high technology readiness levels (TRLs), and viable business cases are the only ones that can be implemented in time.

The time is rapidly approaching when the UK Government will have to ‘pick technology winners’… something it has been fastidiously avoiding for years. Without the Government deciding on which technologies to support and creating the legislative and financial environment to support them, there is little chance of hitting the 2030 target. The Government’s dilemma is exacerbated by the fact that decarbonisation is a complex system problem, with incomplete and contradictory information and many interacting components across the economy. Such problems are sometimes known as ‘wicked problems‘.

It is in this urgent, complex and risky environment that major decisions have to be made about which technologies should power the UK’s future industrial processes, heavy vehicles, heating and cooling systems and electricity storage. The two main contenders for these applications are electricity and hydrogen. This article examines the choice.

The Colours of Hydrogen

Hydrogen can be manufactured in various ways. The resulting H2 gas (which differs only in the level of contaminants) is designated by a colour according to the manufacturing route:

- ‘Green’ Hydrogen is manufactured by electrolysis: using renewable electricity to split pure water into Hydrogen and Oxygen.

- ‘Grey’ Hydrogen is manufactured by Steam Methane Reforming (SMR): using high temperature steam to convert Methane into Hydrogen and CO2. This is how essentially all the world’s Hydrogen is currently made (mainly for manufacture of Ammonia in fertilizer production).

- When the CO2 from the SMR process is captured and stored in permanent underground storage, the output is known as ‘Blue’ Hydrogen.

Green and Blue Hydrogen are considered to be ‘low Carbon’. Grey is not.

The Choices for Decarbonisation

Advocates for a Hydrogen economy generally propose Green Hydrogen to power future energy systems. The idea is that Green Hydrogen will be generated at times of day when renewable electricity is cheap (ie when supply is high and demand is low). The hydrogen will be stored in underground salt caverns until needed and then either converted back to electricity and injected into the electricity grid or piped around the country to heat homes and fuel lorries. With one silver bullet, this imaginative scheme solves the three problems of electricity storage [Article 3], heating of buildings [Article 2] and powering heavy transport systems [Article 1]. Job done!

Some of these advocates recognise that generating and storing Green Hydrogen at the necessary scale is an immense task which would take many decades to achieve. Consequently they propose to use Blue Hydrogen as a ‘stop-gap’ solution until the Green Hydrogen infrastructure can be rolled-out.

Proponents of an ‘electron economy’ propose use of electric heat pumps for heating buildings [Article 2], battery-powered or catenary-powered electric lorries [Article 1] and various possible technologies with high round-trip efficiencies for electricity storage [Article 3]. Hydrogen will still play a part in this electron economy – in places that electrification can’t reach: for manufacture of fertilizer and for some other industrial processes; possibly for aircraft propulsion and in manufacture of ammonia, which is being proposed as a liquid fuel for shipping.

Challenges of Green Hydrogen

Energy Efficiency

‘Energy efficiency’ is the proportion of the energy that enters a system that can be put to useful effect. For example, an efficiency of 0.4 or 40% (as can be achieved by a modern diesel engine) means that 40% of the input energy from the fuel is converted into useful work and consequently 60% of the input energy is lost in the process, as low-grade heat. This can be written mathematically as:

N = Eo/Ei

where: N is the energy efficiency, which takes values between 0 and 1.0 (or 0% to 100%); Ei is input energy: Eo is the output energy.

If the output energy requirement is known, this equation can be used to estimate the amount of input energy needed to power the system. For example, we know approximately how much heat is used to heat all buildings in the UK (‘Eo’ in this case) from their natural gas consumption, and we know the energy efficiencies (‘N’) of various process paths to generate heat energy from renewable electricity – eg via hydrogen boilers or heat pumps. Therefore we can calculate the amount of renewable electricity required to power the heating systems (‘Ei’) via each of the pathways, by rearranging the above equation to give:

Ei = Eo x (1/N)

If the efficiency is low, ie N is significantly less than 1, its ‘reciprocal’ 1/N is large. (The function 1/N is known as a hyperbola – it becomes very large as N approaches zero).. For example, if N = 0.4 (ie the system is 40% efficient), then 1/N = 2.5. This means that 2.5 times more energy is needed for input to the process (Ei) than is available at output for useful effect (Eo). If N = 0.2, then 1/N = 5… so 5 times more energy is needed for input to produce a given output.

Conversely if the system efficiency is high so that N is near 1.0 then 1/N is a little more than 1.0. For example, if N = 0.9 (90% efficient), then 1/N =1.11… ie only 11% more energy is needed for input to produce a given output. So while the efficiency N is often quoted by engineers, it is actually (1/N) that matters when evaluating the amount of renewable energy needed to fuel the system.

Why does this matter? Because in a future renewable world, powered entirely by low-Carbon energy sources, you can’t just pour 4 times more high energy fuel ‘fossil Ei’ into a fuel tank. You have to build 4 times more wind turbines or 4 times more solar panels or 4 times more nuclear power capability, which costs a lot of money and time – both of which are in short supply in the climate crisis. Energy efficiency is not just a geeky engineering concept. It is a central factor in any rational decision involving energy systems.

Energy efficiency is also important for the national economy. If the nation is profligate in its use of energy, people pay higher heating bills and transportation costs to energy providers. Consequently there is less money to go around and the economy suffers. If the nation is efficient in its use of energy, money is available for other personal expenditure or to pay tax, benefitting the economy. So national decisions about energy systems also have significant economic consequences.

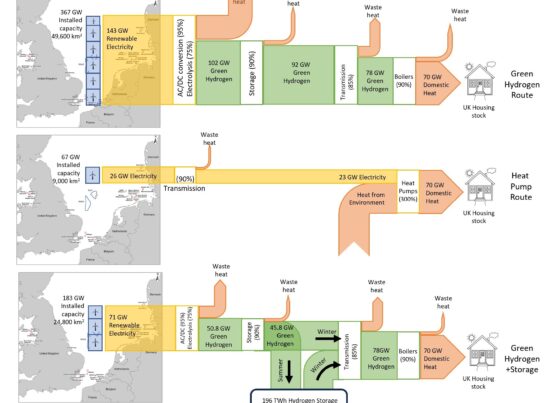

Low efficiency is the Achilles’ heel of processes involving Green Hydrogen. If Green Hydrogen is used to power systems, a large amount of renewable electricity is needed as input to overcome the high inefficiencies in electrolysis, compression, storage, pumping and converting the hydrogen back to electricity in fuel cells. For example: If you produce Green Hydrogen and use it to power a lorry, the efficiency from ‘windmill to wheel’ is about 0.23 (23%) [Article 1]. That means every 1kWh of power needed to move a lorry takes 1/0.23 = 4.4 kWh of renewable electricity. Conversely if you use the electricity directly to power lorries on an Electric Road System, the equivalent efficiency is about 0.77 (77%) [Article 1]. This means that every 1 kWh at the wheels uses 1.3 kWh of renewable electricity. So the Green Hydrogen route would use 4.4/1.3 = 3.3 times more renewable electricity to power the nation’s lorries.

These inefficiencies are intrinsic to the processes because they are caused by fundamental limits of thermodynamics. This means that while small incremental improvements in individual process steps may be possible by clever engineering, the highest possible efficiencies are constrained by thermodynamic limits that can’t be exceeded. Consequently, the inefficiency problems can’t be ‘cured’ by technological advances.

Green Hydrogen suffers from very poor efficiencies in each of the applications described in Articles, 1, 2 and 3:

- For powering the UK’s lorries: 3.3 times more renewable electricity would be needed for Green Hydrogen than for electricity [Article 1]. This factor of 3.3 could be reduced a little through improved engineering, but it is never going to go below about 3 for the thermodynamic reasons explained above.

- For heating the UK’s buildings: 6 times more renewable electricity would be needed for Green Hydrogen boilers than for heat pumps [Article 2].

- For electricity storage: The ‘break even price’ of electricity stored via Green Hydrogen would be 2.2 times higher than electricity stored by more efficient storage systems such as cryogenic or compressed air storage [Article 3]

None of these factors (3.3, 6 or 2.2) are likely to change significantly through future engineering advances. They are constants that political decision-makers can rely-upon.

Figure 2 from [Article 2] illustrates the second of these points. If the UK’s heating needs were satisfied using electric heat pumps, 67 GW of additional renewable electricity would be needed and this could be provided by 5,600 additional 12MW offshore wind turbines. These would occupy an area of sea shown to scale by the blue circle on the figure. Building all of these turbines would be a very large, expensive challenge.

If Green Hydrogen was burned in condensing boilers to heat the UK’s buildings, 385GW of additional renewable electricity would be needed to supply the electricity to generate the Green Hydrogen and overcome the inefficiencies. This would require 32,000 offshore wind turbines, which would occupy the area of sea shown to scale by the green circle.

Of course, in this example the issue is not just the area of land or sea needed for renewable energy generation:

- Six times more money (capital and running costs) would be needed to generate the electricity, which means the energy cost of heating by hydrogen boilers would be six times higher than providing the same amount of heat using heat pumps.

- The additional energy cost would carry significant economic consequences. Either consumers would have to pay much higher heating bills, or Government would have to subsidise hydrogen costs for the foreseeable future. Either would heavily hit the nation’s financial bottom line.

- Similar arguments can be used to compare hydrogen-powered and electric heavy goods vehicles – see [Article 1]. In this case, the high energy costs of manufacturing Green Hydrogen would mean that the energy costs of hydrogen-powered vehicles would probably be 3.3 times more than electric lorries.

Conclusion: Inefficiencies in production, compression, storage, transport and conversion to electricity in fuel cells make Green Hydrogen economically unattractive compared with direct electrification: for heating, freight transport and energy storage.

Conclusion: A Green Hydrogen economy would require vast amounts of renewable electricity generation: much more than can reasonably be contemplated into the long distant future.

Scaling Green Hydrogen Production

Although the technologies for Green Hydrogen production, storage and distribution exist, they have never before been scaled to the quantities required:

- Building such a large amount of renewable electricity generating capacity would take decades. The amount required far exceeds that previously anticipated by the industry in the planned installation at ‘Dogger Bank’ (see blue polygons labelled ‘East’ and ‘West’ on Figure 2) . During the scale-up period, mitigation of other carbon emissions- eg decarbonising the electricity grid – is likely to be severely compromised, preventing the 2030 and 2050 targets from being met.

- The technology for electrolysis at scale is far from ready for prime time. The “world’s largest electrolysis plant” was completed in March, 2020, by Toshiba in Japan. It has a capacity of 10 MW – a little less than the power of one 12MW offshore wind turbine. The equivalent of about 28,000 such electrolysers would need to be installed in the UK by 2030 to hit the 68% CO2 reduction target for heating buildings and powering long-haul lorries using Hydrogen.

- According to the 2019 International Energy Association report ‘The Future of Hydrogen’ [2] there are 3 suitable salt cavern sites for hydrogen storage in the USA and another 3 sites in the UK. The report also says there is “little experience with depleted oil and gas fields or water aquifers for hydrogen storage (e.g. contamination issues)”. This raises questions about whether the storage available is anywhere near sufficient in quality or quantity to meet demand. Hydrogen storage at this scale is completely undeveloped. There are no examples or prototype systems in existence. Its technology readiness is near the lowest level on the TRL scale. It is clearly not ready for prime time.

The magnitude of these issues associated with Green Hydrogen scale-up has either not been thought-through or is being deliberately underplayed by Hydrogen advocates. It is highly doubtful whether decarbonisation via the ‘silver bullet’ Green Hydrogen route could be achieved in any time-scale.

Conclusion: A Green Hydrogen economy in the UK, as is being advocated by the Hydrogen Lobby, is a deeply flawed concept with little prospect of delivery.

Challenges of Blue Hydrogen

So if Green Hydrogen can’t be scaled in time to solve the decarbonisation problem, what about Blue Hydrogen?

Technology Readiness

The key components of any Blue Hydrogen system, that would have to be ‘68% complete’ by 2030 are:

- Hydrogen generation by Steam Methane Reforming (SMR)

- Carbon capture and storage (CCS)

- Hydrogen distribution via pipelines or tankers.

- Hydrogen end-uses: hydrogen boilers and fuel cell electric vehicles (FCEVs)

SMR

SMR is a mature, scalable process. It is used for Grey Hydrogen production worldwide: for manufacture of fertilizer and for other industrial processes such as gas to liquid hydrocarbon fuel manufacture. Production of Grey Hydrogen generates approximately 830 Mt of CO2 per annum (Mt/a) globally. However according to the Global CCS Institute’s database of CCS facilities there are only two operating, commercial-scale SMR plants in the world with integral CCS for making Blue Hydrogen. Between them, these two plants sequester a total of 2 Mt/a of CO2: about 0.24% of current global Hydrogen production. So the Hydrogen industry has a long way to go before current Hydrogen manufacture can be considered ‘clean’. Perhaps this would be a good place to start before proposing to take over fuelling of heating and road transport as well?

CCS

Large-scale CCS is far from being ready for prime-time. The world’s total Carbon sequestration capacity is currently less that 0.1% of global CO2 emissions and there is no commercial-scale CCS facility in the UK or the EU. It would have to be developed before any Blue Hydrogen could be generated. You can find an informative discussion about world CCS capacity in this article.

The only financially-viable CCS projects in the world inject CO2 into oil wells to enhanced oil recovery (‘EOR’). Other CCS projects are not viable because of low Carbon prices, see [Article 2]. Consequently large-scale CCS could only occur through imposition of high Carbon taxes in the UK or major Government subsidies. The amount of CCS needed in the UK to get to 68% decarbonisation of heat and HGVs by 2030, using a Blue Hydrogen route is around 35 Mt/a. This would require the UK to build the equivalent of five of the largest CCS plants currently in existence by 2030 [Article 2].

Furthermore, SMR+CCS (Blue Hydrogen) is not a ‘zero Carbon’ option. CCS can, at best, only capture 90% of the CO2 in the exhaust stream of the SMR process. At least 10% of CO2 will escape into the atmosphere (see [Article 2]). And, of course, large fugitive emissions of Methane occur throughout the natural gas processing supply chain. This is non-trivial: The International Energy Agency (IEA) reported that in 2020, the oil and gas industry leaked over 70 million tonnes of methane into the atmosphere. According to Bloomberg Green, these fugitive Methane emissions were equivalent to Europe’s entire Carbon Footprint. These emissions are very damaging to the environment, because Methane is 25 time more potent a greenhouse gas than CO2 when assessed on a 100 year timescale and 86 times more potent a greenhouse gas than CO2. when assessed on a 20 year timescale

So the Blue Hydrogen route will never be clean and it will never be able to provide ‘Net Zero’ Carbon emissions. Consequently, any investment in Blue Hydrogen production will have a finite life and will eventually have to be written-off so that Green Hydrogen generation can be rebuilt in its place. This will discourage investment in Blue Hydrogen.

Conclusion: Given the low technology readiness of commercial-scale CCS, it is highly unlikely that the Blue Hydrogen production needed to power 68% of long-haul lorries and 68% of building heat could be implemented in the UK by 2030, 2040 or 2050.

Grey Hydrogen

If Hydrogen is needed for lorries and heating in the short term, and Green and Blue Hydrogen can’t be manufactured in time, it seems clear that the Grey Hydrogen industry (which has a much cheaper product than Blue or Green Hydrogen) will step-up to the supply challenge…

Using Grey Hydrogen is the worst thing to do. Not only is all of the Carbon in the Methane converted into CO2 and released into the atmosphere, but the low efficiencies of the hydrogen processes means that considerably more Methane is needed to fuel the same vehicles and heating systems. This will result in significantly higher CO2 emissions than burning natural gas directly. For example, using data from [Article 2], burning Grey Hydrogen in a condensing boiler will generate approximately 0.62 kgCO2/kWh of heat delivered (‘Well-to-Boiler’). On the same basis, burning natural gas directly in a conventional condensing boiler generates approximately 0.22 kgCO2/kWh of heat delivered. So using Grey Hydrogen instead of natural gas will generate about 0.62/0.22 = 2.8 times higher Carbon emissions to heat the same buildings.

Performing similar calculations for lorries using data from [Article 1] shows that using Grey Hydrogen in fuel cells will generate approximately 0.96 kgCO2/kWh of power delivered by the lorry (Well-to-Wheel), whereas burning natural gas directly in an internal combustion engine generates about 0.67 kgCO2/kWh. So the Grey hydrogen route generates about 40% higher Carbon emissions than burning natural gas directly.

Conclusion: Use of Grey Hydrogen will make emissions much worse than burning natural gas directly (ie doing nothing). Policy makers should beware of the detrimental effects on Carbon emissions of inadvertently promoting Grey Hydrogen consumption because Blue or Green Hydrogen are not ready for prime-time.

Hydrogen Distribution

Hydrogen has a significantly lower energy content per unit volume (‘Lower Calorific Value’ LCV=10.8 MJ/m3 ) than Methane (LCV=35.8 MJ/m3 ) [Article 1]. The factor of 35.8/10.8 = 3.3 means that transferring the same amount of energy to consumers using Hydrogen instead of Methane, would require all gas pipes in the system to carry 3.3 times higher volume flow rate of gas. This means that many pipes in the gas transmission system would need to be replaced with pipes of significantly larger diameter.

Furthermore, about 3-4 times more power (and different pumps) would be needed to pump hydrogen as the same amount of energy via natural gas [3], [4]. According to Martin, [4], this explains why hydrogen isn’t generally moved around by pipeline. Instead, natural gas is moved to where the hydrogen is needed and the SMR process is implemented there. Of course those deciding on the location of SMR plants also need to consider that, every 1 kg of Blue Hydrogen manufactured by SMR generates 9 kg CO2 which has to be transported from the SMR plant to the sequestration point, by pipeline or heavy goods vehicles.

Conclusion: Distribution of Hydrogen through the National Transmission System (gas grid), would require much of the infrastructure to be replaced and would use 3-4 times more pumping energy than pumping the equivalent amount of natural gas.

End uses: Hydrogen-ready Boilers, FCEVs

Prototype Hydrogen-ready condensing boilers exist. Their development and scaling is not thought to be a barrier to rolling out hydrogen for heating buildings.

A few prototype fuel-cell powered lorries have been built. These can most likely be commercialised by 2030. However the prices are expected to be high. For example, in the US, the Nikola Motors tractor unit is expected to sell for about three times the the price of a conventional diesel vehicle. (NB: This estimate was made before various scandals that question the legitimacy of Nikola’s technology and business.)

Conclusion: Hydrogen Boilers and FCEVs could be made ready for widespread use by 2030, but the infrastructure that provides low-carbon hydrogen could not.

Additional Methane Requirements

Figure 3 shows the total flows of natural gas in the UK in 2019, from UK government statistics [5]. On the left, it can be seen that the UK produced 439 TWh and imported 518 TWh of natural gas: ie 54% of total gas consumption was imported. The bottom right of the figure shows that 124 TWh of methane would be needed to power lorries (calculated in [Article 1]) and 135 TWh would be needed for heating buildings (calculated in [Article 2]). This gives a total additional gas requirement of about 260 TWh. Since domestic gas production is declining, this additional gas would have to be imported.

If 260 TWh of methane was added to the imports, they would increase by 50% to 777 TWh or 64% of the total. Based on an average wholesale price of £0.50 per ‘Therm’ [6], the 260 TWh of additional gas consumption, would drain an additional £4.4b from the UK economy each year: directly to the gas producers. The retail cost to consumers would be significantly higher than £4.4b, and of course, this same economic impact would be repeated in every country that adopts a blue hydrogen economy. So it is not surprising that the fossil fuel industry is actively promoting Hydrogen as the solution to the world’s ‘low carbon’ energy needs. (See [7] and [8]).

This increase in gas imports would cause a significant dent in the UK’s balance of trade and would have a detrimental effect on the country’s energy security.

Conclusion: Shifting the energy requirement for lorries and heating to Blue Hydrogen would result in the UK importing and burning an additional 260 TWh of natural gas per year. This would increase gas imports by 50%. It would damage the country’s balance of trade and energy security.

Electrification

So what about the alternative to Hydrogen in these applications: electrification?

Electricity Generation and Distribution

Using the calculations in [Article 1] and [Article 2], it would be necessary to install about 80 GW of additional offshore wind electricity generating capacity to: (i) power the UK’s lorries by electricity and (ii) heat all of its buildings using heat pumps. This would be a major task, but would be a factor of 5 less the 420 GW of additional renewable electricity needed to power these systems by Green Hydrogen.

It would be necessary to reinforce the electricity grid to handle higher loads in some locations. Though again, this would be much less than the grid reinforcement needed for Green Hydrogen.

Heat Pumps

Heat pumps are standard, mature, off-the shelf technology that can be purchased now [Article 2]. There are currently 220 million heat pumps in use around the world. They come in two main varieties: ‘air-source’ heat pumps (ASHP) and ‘ground-source’ heat pumps (GHSP). ASHPs are better for retrofitting existing buildings. GSHPs are more efficient, though more expensive and can be installed in new buildings most easily. Heat pumps are most effective when used in well insulated buildings.

Conclusion: Electric Heat Pumps are widely available worldwide and can be deployed reasonably easily in the UK.

Electric HGVs and Electric Road Systems (ERS):

[Article 1] explains that ERS technology, particularly the ‘eHighway’ version which uses overhead catenary cables contacted by pantographs carried on the vehicles, is well developed and has been tested in 4 major highway trials in the past few years.

A detailed analysis of the implementation of an electric road system for UK lorries is available in a White Paper by the Centre for Sustainable Road Freight [9]. The White Paper shows that:

- The first phase of the proposed eHighway construction in the UK could be completed by 2030.

- When combined with the rapid roll-out of battery electric vehicles for urban delivery, currently occurring in the industry, a total of about 60-65% of lorry kms in the UK would be electrified. This is close to the 68% 2030 target (based on 1990 levels).

- The remaining eHighway network could be deployed by 2040: effectively decarbonising all of the UK’s heavy goods vehicles.

- The cost of this deployment of eHIghways over the entire major road network of the UK is estimated to be about £20b, which is comparable with £28.8b announced in the UK Government’s 2018 Budget for the ‘National Roads Fund‘ for spending on roads in 2020-2025; and about 1/5 of the projected cost of the HS2 railway project.

- The vehicle technologies needed are mature and can be rolled-out by 2030. The series hybrid and battery electric vehicles could all have batteries with capacities of 100kWh or less and would carry active pantograph mechanisms on their roofs.

The White paper also analyses the three main business cases associated with an eHighway system and concludes that the following could be all be funded simultaneously through electricity sales to vehicle operators:

- Vehicle owners could have an 18 month payback period for the additional cost of purchasing catenary-electric lorries compared to conventional diesels, due to their low operating energy costs. This would ensure rapid take-up of electric lorries by the industry.

- Private infrastructure providers could pay back the cost of building the eHighway infrastructure in 15 years, with an appropriate return on borrowed capital, using revenue from electricity sales to lorries.

- Central government could recoup current levels of excise duty from HGV diesel sales by adding a tax to the cost of electricity purchased from the eHighway system.

Conclusion: Electric HGVs are rapidly entering mainstream production for urban delivery and have been widely tested for long-haul operation, powered by catenary cables.

Conclusion: Installation of an Electric Road System in the UK is feasible and economically attractive for fleet operators, infrastructure providers and the Government. This strategy could decarbonise 60-65% of UK lorry kms by 2030 and 100% of UK road freight by 2040.

Electricity Storage

[Article 3] demonstrates the importance of high round-trip efficiencies in the economics of electricity storage, and shows that this rules-out Green Hydrogen storage as an economically viable option. The most likely candidates for grid-scale intra-day storage are cryogenic (liquid air) and compressed air storage. Both can be built at grid scale, and have round-trip efficiencies nearing 70%, compared with around 32% for Green Hydrogen. Liquid Air storage has a high technology readiness level (TRL), with large-scale commercial plants currently under construction. It is safe and benign, uses standard off-the-shelf components and can be located anywhere in the country, on a small area of land… no need to be near salt caverns.

Conclusion: Cryogenic (Liquid Air) storage of electricity is far more efficient, financially attractive and higher technology readiness than electricity storage via Green Hydrogen. Unlike Green Hydrogen, Cryogenic energy storage can be located wherever it is needed and does not need to be located near to salt caverns. It could be rolled-out at scale by 2040.

Confusion and Delay

It has been shown in this article that a Hydrogen economy is a poor choice for decarbonising the UK compared with direct electrification. So why is there suddenly so much interest in Hydrogen?

Peer-reviewed research by Lowes et al [7] showed that there is currently a concerted effort by an international ‘discourse coalition’, “primarily of gas industry incumbents, [who are] under threat from the decarbonisation of heating” and that “the green gas storyline is being oversold by incumbents.” (See also [8].)

In other words, the international fossil fuel industry, which is under existential threat from electrification, is hyping-up hydrogen as a solution, in order to create confusion among politicians and the public and delay its own demise. Undoubtedly the main players understand that a hydrogen economy cannot deliver on their promises. They know that Green Hydrogen is a deeply flawed concept (as explained here). Consequently they are pursuing a ‘bait and switch’ strategy in which they promise a ‘silver bullet’ Green Hydrogen future but then fall back to an interim Blue Hydrogen position which will consume a vast amount of additional natural gas. They know that Blue Hydrogen will take decades of development for deployment at sufficient scale, but during this period they can sell cheaper Grey Hydrogen instead. They ignore the fact that this will make CO2 emissions considerably worse than the status quo (ie just burning natural gas). This delay will give the fossil fuel industry a (temporary) reprieve. They also know that they won’t be able to deliver the promised net-zero future because Blue Hydrogen production will always leak at least 10% of the CO2 into the atmosphere and will also generate fugitive Methane emissions.

It is probable that the Hydrogen Economy project will fail in the end. Hydrogen solutions are too expensive to compete with electric solutions. Just as the free market has rejected hydrogen-powered cars because of their excessive energy costs, so too the market will conclude that hydrogen-powered lorries, hydrogen-powered heating and Green Hydrogen electricity storage are all too expensive to compete with energy-efficient electrical alternatives. Unfortunately, this will take some years to play out. In the meantime, encouraged by the Hydrogen hype, the government will continue to subsidise hydrogen projects and technology development and the Hydrogen Lobby will continue to obfuscate its fundamental lack of competitiveness.

Conclusion: The Hydrogen Lobby’s ‘confusion and delay’ tactics threaten to derail efforts to decarbonise the nation and the world.

Overall Conclusions

Through this article and the three more detailed analyses of long-haul lorries, heating buildings and electricity storage, I have attempted to provide an objective, quantitative comparison of the Hydrogen and Electron economies. The calculations are all transparent: all of the sources of information are cited and assumptions have been clearly stated.

To me, the outcome is very clear…

The proposed Green Hydrogen economy does not make sense. The amount of sustainable electricity required for heating buildings and powering lorries – and its considerable cost – makes Green Hydrogen a complete non-starter. Green hydrogen doesn’t make sense as a storage mechanism either – because the round-trip efficiency is so low that it could never compete on price with alternative, higher TRL storage systems.

The fall-back Blue Hydrogen strategy appears to be a cynical ploy by the fossil fuel industry to sell a great deal of additional natural gas, while sowing confusion in political and public minds and thereby causing dangerous delay to the international decarbonisation project.

If the UK government is serious about decarbonisation, it should pursue a strategy of electrifying everything possible, as soon as possible. That includes all land transport and heating of buildings. There will need to be a commensurate large-scale increase in sustainable electricity generation. There should also be a strong emphasis on energy efficiency, through insulation of buildings, encouraging various measures to make freight transport more efficient, as well as other measures throughout the economy. Hydrogen should only be used for the applications that cannot be electrified. This includes fertilizer production, some industrial processes and possibly aviation and shipping…

Postscript – A Personal View

At the end of all this analysis, the question faced by individuals, politicians and the nation as a whole is about the type of world to which we aspire.

On the one hand, we could have a hydrogen-powered future: a high energy, high consumption, high cost economy; in which we decarbonise slowly, burn large amounts of fossil fuels and/or have to generate eye-watering amounts of renewable energy to create hydrogen. If it could be achieved, this Hydrogen economy would provide systems that are familiar: replacing natural gas boilers with Hydrogen boilers to heat our homes and having lorries that can refuel quickly and travel anywhere.

On the other hand, we could have an electrical future: a relatively low energy, low consumption, low cost economy; in which we decarbonise quickly and conserve renewable energy. This would be in exchange for some changes, like having to replace gas boilers with heat pumps in our homes, slightly less flexible logistics systems and the visual impact of catenary cables strung over motorways.

With the earth at the tipping point of environmental disaster caused by overconsumption of energy, water and natural resources, and a great need to decarbonise quickly, it seems clear to me which approach is better for the planet.

References

[1] Andrew, R. Center for International Climate Research (CICERO), Norway https://folk.universitetetioslo.no/roberan/t/global_mitigation_curves.shtml

[2] Anon ‘The Future of Hydrogen’, IEA, June, 2019, 199pp https://www.iea.org/reports/the-future-of-hydrogen.

[3] Bossel, U. ‘Does a Hydrogen Economy Make Sense?’ Proc. IEEE, Vol 94, No. 10, pp. 1826-1837, Oct 2006. http://DOI.org/10.1109/JPROC.2006.883715.

[4] Martin, P. ‘Hydrogen to Replace Natural Gas- By the Numbers’, LinkedIN, December 6, 2020 https://www.linkedin.com/pulse/hydrogen-replace-natural-gas-numbers-paul-martin/

[5] ‘Digest of UK Energy Statistics (DUKES) 2020’, Chapter 4 ‘Natural Gas’. BEIS, 2020. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/924591/DUKES_2020_MASTER.pdf

[6] Ofgem ‘All wholesale gas charts and indicators’, Accessed 28 Dec, 2020. https://www.ofgem.gov.uk/data-portal/all-charts/policy-area/gas-wholesale-markets

[7] Lowes, R. Woodman, B. and Spiers, J. ‘Heating in Great Britain: An incumbent discourse coalition resists an electrifying future’, Environmental Innovation and Societal Transitions, Volume 37, 2020, Pages 1-17. https://doi.org/10.1016/j.eist.2020.07.007

[8] Balanyá, B. Charlier, G. Kieninger F. and Gerebizza, E. ‘The hydrogen hype: Gas industry fairy tale or climate horror story?’, 47pp, Corporate Europe Observatory (CEO), Brussels, December 2020. https://corporateeurope.org/sites/default/files/2020-12/hydrogen-report-web-final_0.pdf

[9] Ainalis, D.T., Thorne, C., and Cebon, D. ‘Decarbonising the UK’s Long-Haul Road Freight at Minimum Economic Cost’, Centre for Sustainable Road Freight, Technical Report CUED/C-SRF/TR17 July 2020. http://www.csrf.ac.uk/2020/07/white-paper-long-haul-freight-electrification/